The most interesting activity for natural gas report week, October 14, 2021 was the price increase pushing the 12-Month and Summer Strip higher. While prompt month prices rose 9.7 cents from Wednesday to Thursday, week-over-week growth was modest. Even the diminishing Winter Strip gained just 3.1 cents from last week. As such it was certainly attention grabbing to see the largest gains consolidated in months that have, up until this point, seen price movement subdued by anticipation of warm spring weather and expectation of production growth.

So, as the last few months have had us asking when it comes to natural gas prices, why?

Fundamentals + Europe + Russia = ?

Winter natural gas prices have claimed headlines in recent weeks on the realization domestic prices were moving in tandem with skyrocketing European energy markets. Allaying European concerns over storage shortfalls, Russia vowed increased natural gas deliveries. This mollified near-term market volatility, at least for now. Should Russia fail to deliver on their promise, expect volatility in domestic and international natural gas markets to return.

At home, prices for winter months rose dramatically before retreating immediately following the EIA’s publication of this week’s 81 Bcf storage build. But as winter prices calmed, spring shoulder month prices jumped, suggestive of market sentiment that end-of-winter storage inventories could land below the five-year average.

To be sure, with winter fast approaching (sorry, fans of summer) attention has remained on the weather forecast. In short, extreme cold would likely mean higher prices whereas average winter temperatures would help keep the market in check.

Either way, the EIA’s October Short Term Energy Outlook offers a few key insights:

- Inventories will end the 2021 injection season at almost 3.6 Tcf, 5% less than the five-year average.

- Natural gas inventories are estimated to fall by 2.1 Tcf this winter, ending March at less than 1.5 Tcf, 12% less than the five-year average.

- U.S. draws will be slightly more than the five-year average this winter. That, along with rising exports and relatively flat production through January, will keep prices near recent levels before downward pressures emerge.

- Given low inventories in both U.S. and Europe and uncertainty around seasonal demand, natural gas prices will remain volatile over the coming months, with winter temperatures being a key driver of demand and prices.

DEC21, settled at $5.837/Dth, up 2.0 cents

JAN22, settled at $5.936/Dth, up 2.6 cents

FEB22, settled at $5.835/Dth, up 2.9 cents

MAR22, settled at $5.527/Dth up 7.0 cents

APR22, settled at $4.149/Dth up 16.3 cents

Natural Gas Market Report – October 14, 2021

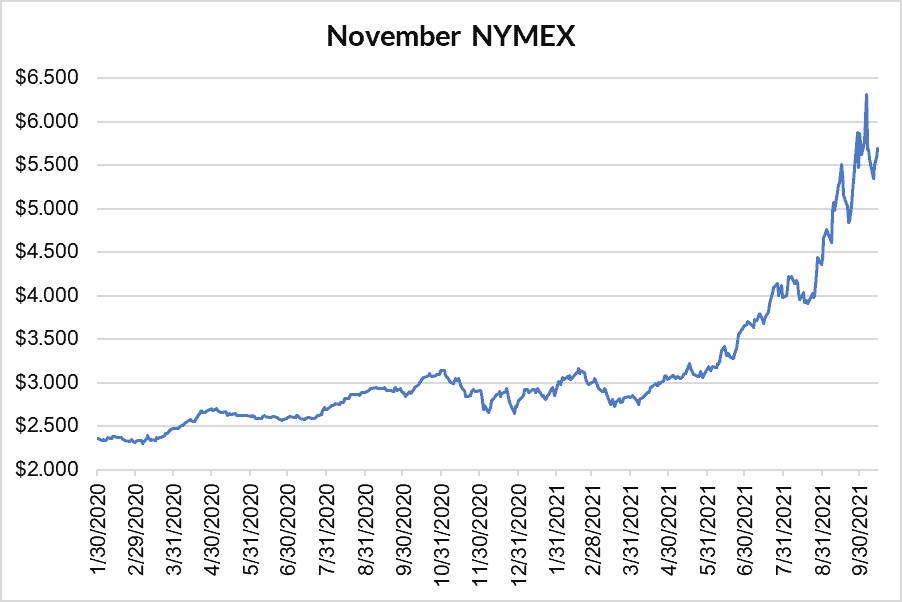

November NYMEX

Settled Thursday at $5.687/Dth up 9.7 cents from Wednesday’s close at $5.590/Dth. Up a penny, week-over-week.

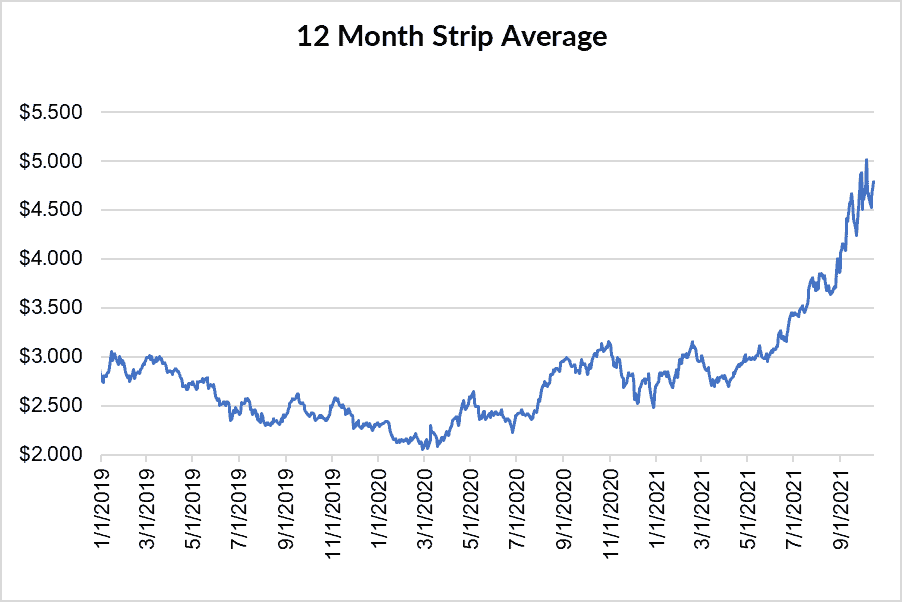

12 Month Strip

Settled Thursday at $4.788/Dth, up 12.1 cents from the prior week.

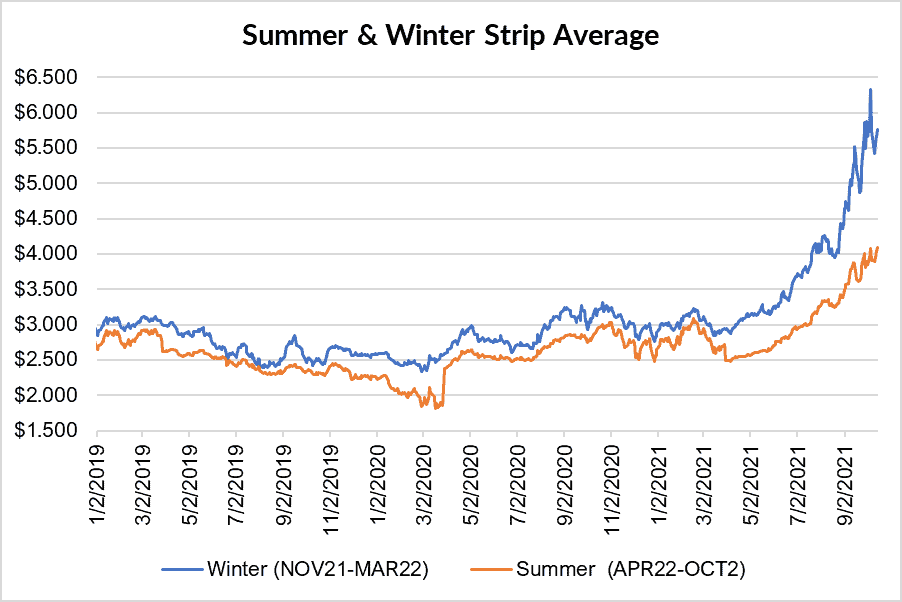

Seasonal Strips

The winter strip (NOV21-MAR22) settled Thursday at $5.764/Dth, up 3.1 cents from the week prior. The summer strip (APR22-OCT22) settled Thursday at $4.090/Dth, up 18.5 cents from the week prior.

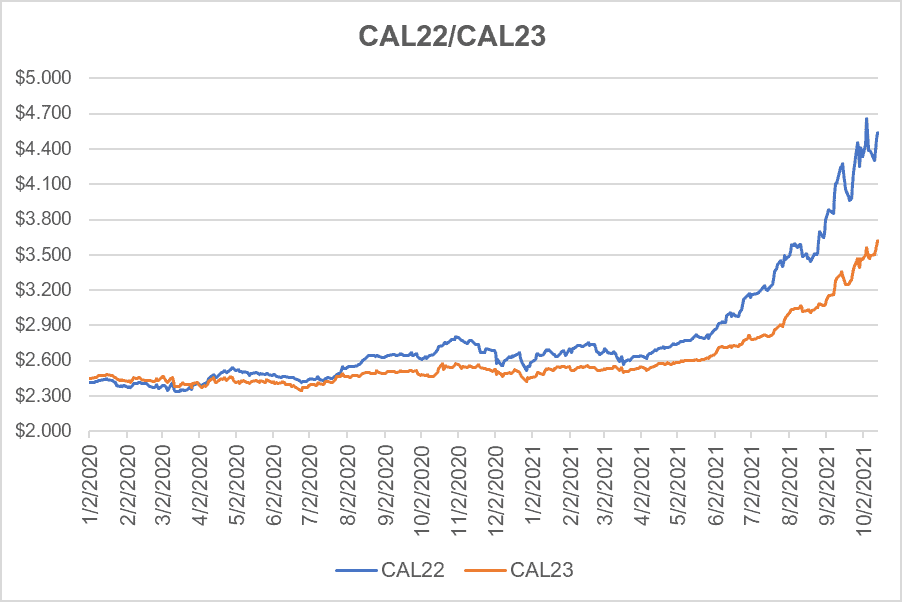

Calendar Years 2022/2023

CY22 settled Thursday at $4.390/Dth, down 2.2 cents from the prior week. CY23 settled Thursday at $3.473/Dth, up less than a penny from the prior week.

Thanks For Sharing!